- info@otsforyou.com

- Mon - Sat: 9:00 - 18:30

INCOTERMS

INCOTERMS FREIGHT

- TACT (The Air Cargo Tariff) : Air Cargo Tariff Book

- FREIGHT PREPAID: Freight with advance payment

- FREIGHT COLLECT : Freight paid by counterparty

- KONSOLİDE : Collect cargo by multiple senders under same waybill

- BREAK BULK : Separation of consolidated cargo

- BACK TO BACK : One-by-one loading. Sending the cargo, belonging to a single consigner, with a single consignee

- DANGEROUS GOODS : Hazardous materials

- HANDLING : Controlling, managing, carrying or using with hand.

INCOTERMS CARRIER

- ICAO(International Civil Aviation Organization): International Civil Aviation Organization

- CONVENTION OF WARSAW: The protocol on international carriage by air signed between several countries, including Turkey, in 1929. In 1955, it was amended by The Hague Protocol. It consists of 41 articles.

- CARRIER : the carrier, Airline

- FORWARDER : Organizing firm that conducts operation of land rout, airline and railway carriage, as well as related insurance services through an active network of agencies

- AIRWAYBILL : Air consignment note

- Master AWB / House AWB : Main consignment / Intermediary consignment

- CASS (Cargo Account Settlement System) : System to monitor accounts between CASS member airlines and their IATA cargo agencies

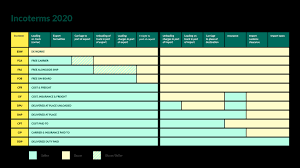

Exclusive rules for sea-freight and inland transport

Abbreviation | Abbreviation | Applicable Transport Type |

|---|---|---|

| FAS | Free Alongside Ship | Seafreight, inland |

| FOB | Free On Board | Seafreight, inland |

| CFR | Cost And Freight | Seafreight, inland |

| CIF | Cost, Insurance And Freight | Seafreight, inland |

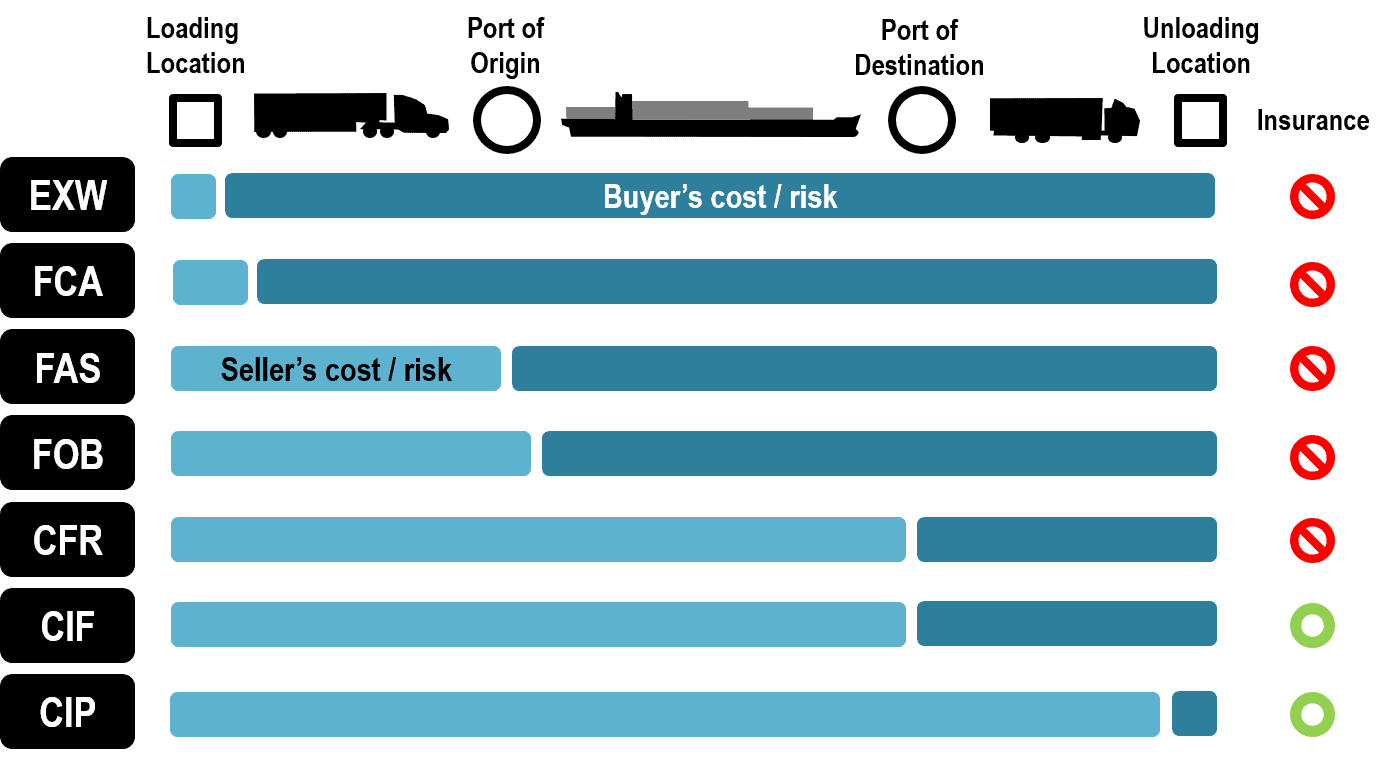

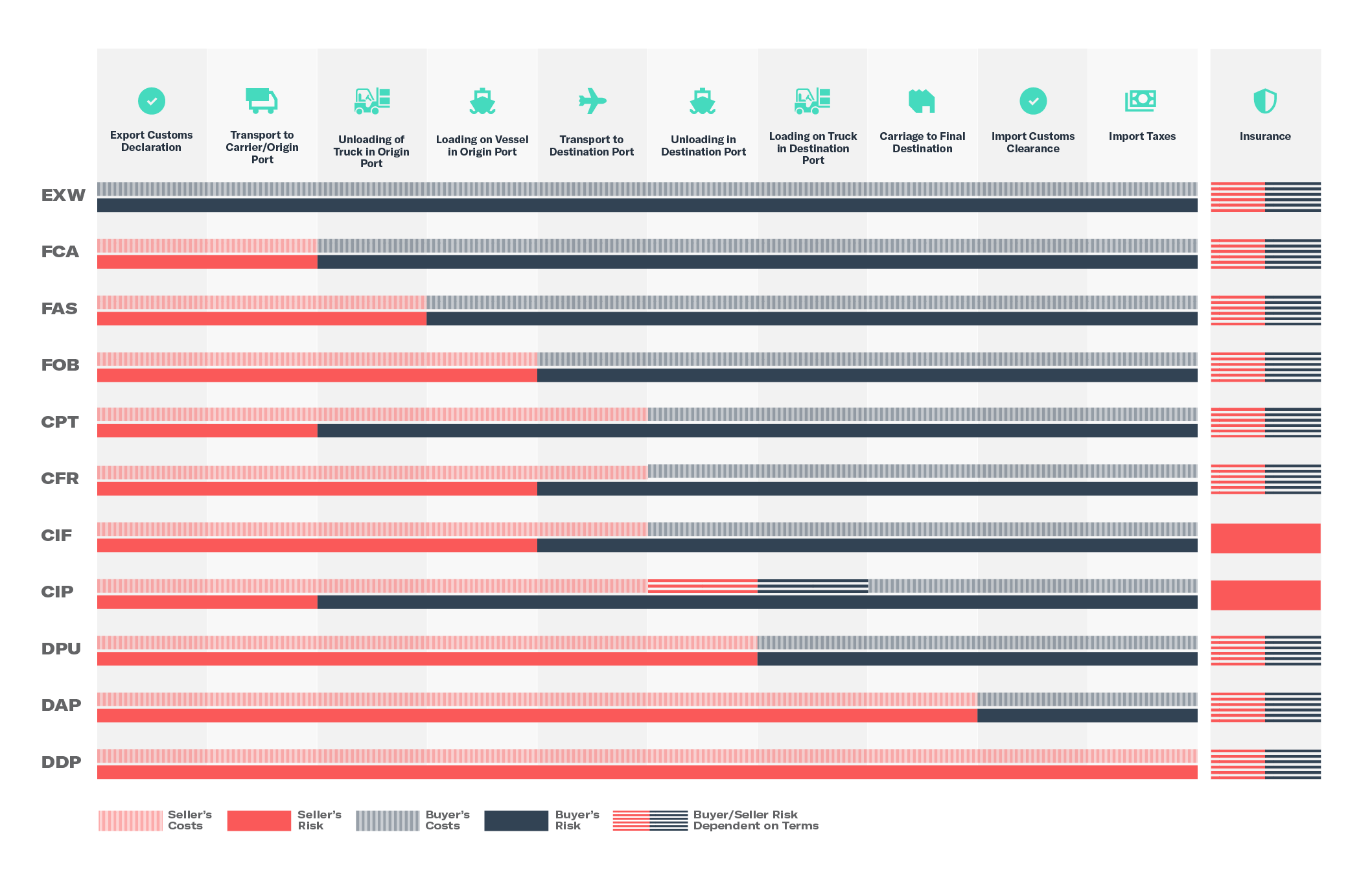

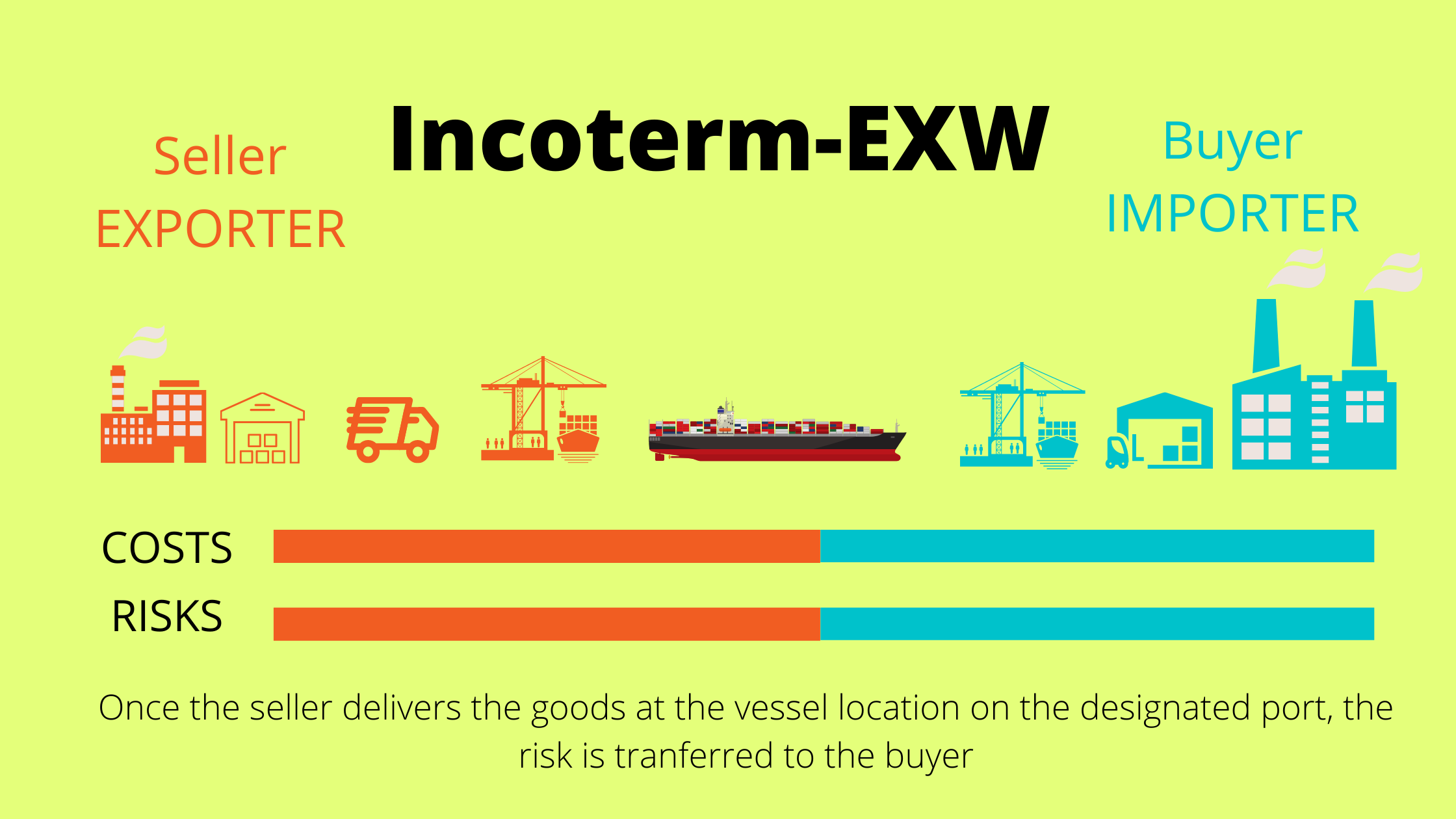

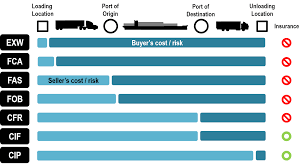

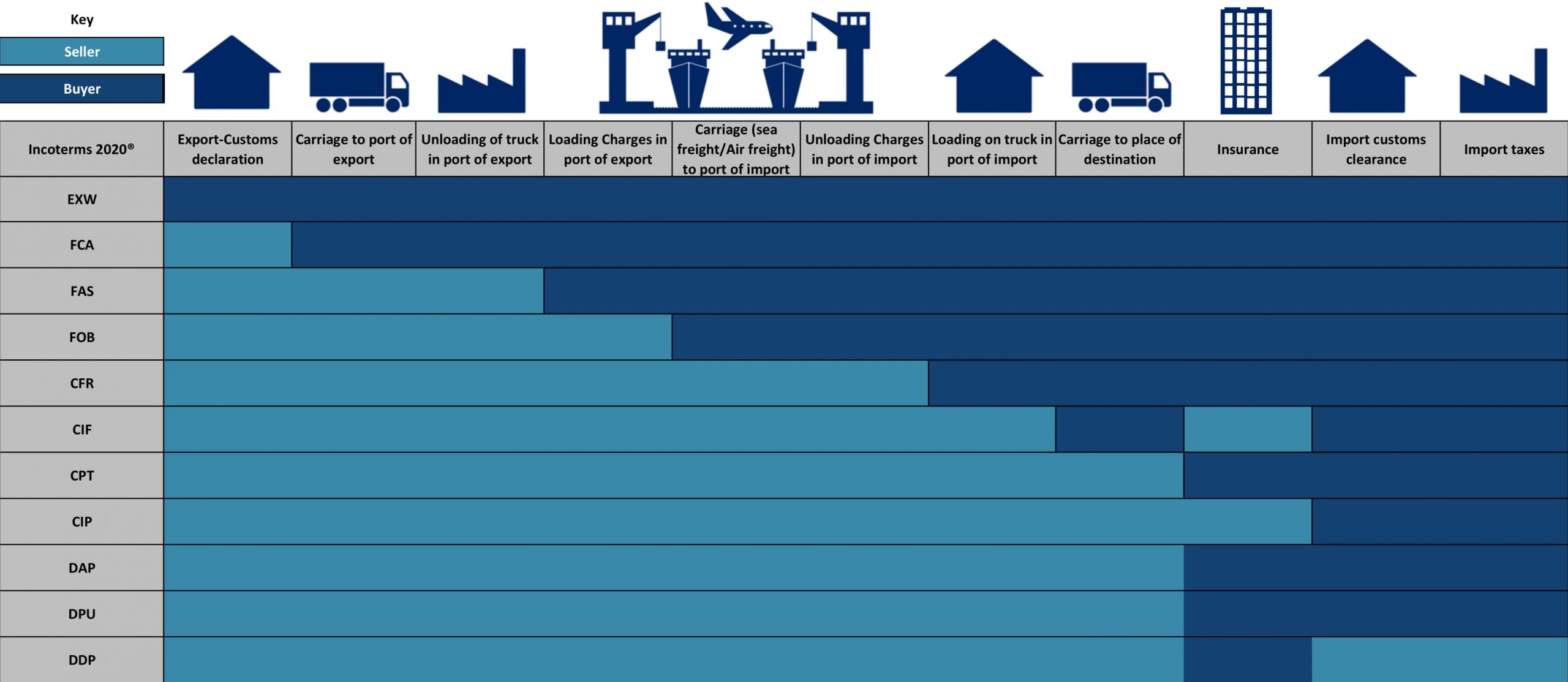

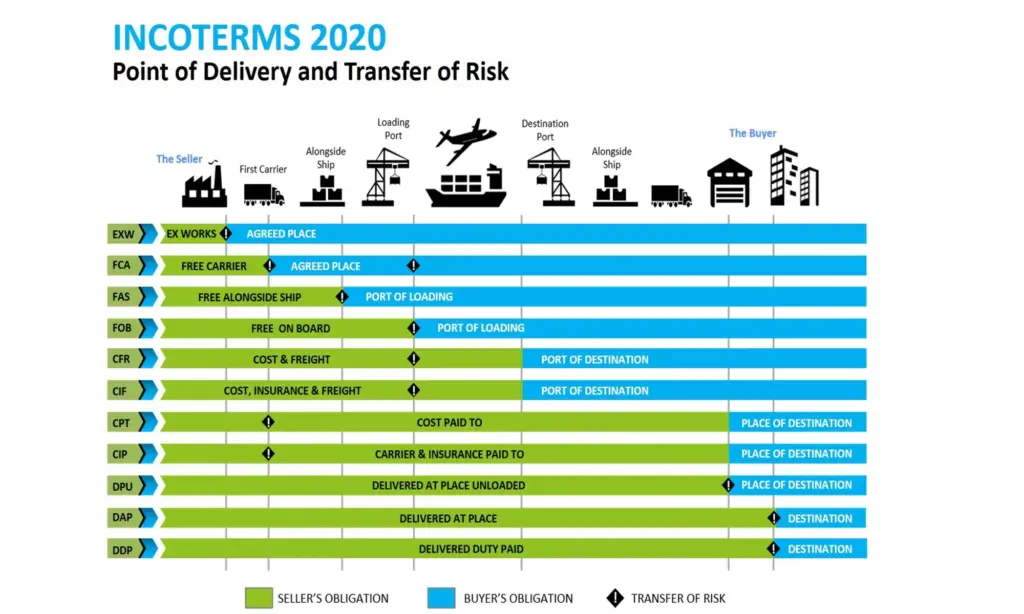

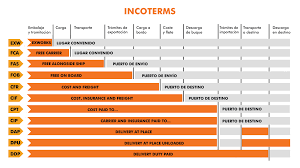

EX WORKS (EXW) /DELIVERY AT COMMERCIAL ENTERPRISE

“Ex works” means the seller fulfils delivery obligation by keeping the goods at its workplace (factory, storehouse etc.) for purchaser. Unless otherwise agreed, the seller is not responsible for loading the goods to a vehicle provided by purchaser or for clearing the goods through export customs. The buyer undertakes responsibility for any expenses and risks about the carriage of goods beginning from the workplace of seller until the destination. This type of sale comprises least liability for seller among all other methods.Only the packaged goods are included within the sale price indicated under the contract in this delivery type. In other words, as of delivery date, the buyer covers all expenses with regard to transport, loading, unloading and insurance.

FREE CARRIER (FCA) / DELIVERY TO CARRIER

In this type of delivery, the delivery liability of seller ends once the goods are cleared through export customs and delivered to the prescribed carrier at the prescribed site or point.

In case the buyer has indicated no precise place of delivery, the seller may determine a site near where the carrier will receive the goods. In case commercial applications require assistance by seller for establishment of a contract with the carrier (e.g. in railroad and airway carriage), the seller may act in such manner that all risks and expenses are covered by the buyer.

INCOTERMS – INTERNATIONAL DELIVERY MODES

| Abbreviation | Full meaning | Applicable Transport Type |

|---|---|---|

| EXW | Ex Works | Road, Airline, Railway, multi-vehicle transport |

| FCA | Free Carrier | Road, Airline, Railway, multi-vehicle transport |

| CPT | Carriage Paid To | Road, Airline, Railway, multi-vehicle transport |

| DAT | Delivered At Terminal | Road, Airline, Railway, multi-vehicle transport |

| DAP | Delivered At Place | Road, Airline, Railway, multi-vehicle transport |

| DDP | Delivered Duty Paid | Road, Airline, Railway, multi-vehicle transport |

| CIP | Carriage And Insurance Paid To | Road, Airline, Railway, multi-vehicle transport |

FREE ALONGSIDE SHIP (FAS)

“Free Along-side Ship” means the seller delivers the goods when they are placed alongside a ship at prescribed port of loading. As of then, the buyer undertakes any expenses, damages or losses, as well as relevant risks about the goods.

FAS requires customs clearance of goods by the seller for exportation.

IT IS THE OPPOSITE OF PREVIOUS INCOTERMS VERSIONS THAT STIPULATE FULFILLMENT OF CUSTOMS CLEARANCE PROCESSES FOR EXPORTATION BY THE BUYER.

- ICAO(International Civil Aviation Organization): International Civil Aviation Organization

- CONVENTION OF WARSAW: The protocol on international carriage by air signed between several countries, including Turkey, in 1929. In 1955, it was amended by The Hague Protocol. It consists of 41 articles.

- CARRIER : the carrier, Airline

- FORWARDER : Organizing firm that conducts operation of land rout, airline and railway carriage, as well as related insurance services through an active network of agencies

- AIRWAYBILL : Air consignment note

- Master AWB / House AWB : Main consignment / Intermediary consignment

- CASS (Cargo Account Settlement System) : System to monitor accounts between CASS member airlines and their IATA cargo agencies

FREE ON BOARD (FOB) / DELIVERY ON BOARD

In this method, the seller is considered to have fulfilled its liability of delivery once the goods reach the ship’s rail at prescribed port of loading. From then on, buyer undertakes any expense, loss, damage or risks about the goods. In case the ship rail signifies nothing in practice (such as in roll-on/roll-off or container carriage), the term FCA will be more appropriate to employ

COST AND FREIGHT (CFR)

In this method, the seller has to pay all relevant costs and freight in order to dispatch the goods to prescribed port of destination. Nevertheless, any loss and damage risks as well as possible rise in expenses with regard to goods are handed over from seller to buyer once the goods attain the ship’s rail at port of loading.

CFR signifies that the seller should clear goods through customs for export.

DELIVERED EX QUAY(DUTY PAID) (DEQ)

(On the condition of indicating port of destination as …) "Delivered ex quay" means that the seller delivers goods to the disposal of buyer at the quay of prescribed port of destination, without fulfilling necessary customs procedures for import. The seller has to undertake all damages and expenses with respect to carriage of goods to prescribed port of destination and their unloading at the quay. DEQ stipulates that the goods are cleared through customs for import and all relevant procedures, taxes, levies and duties are paid by the buyer.

IT IS THE OPPOSITE OF FOREGOING INCOTERM VERSIONS STIPULATING THAT THE BUYER HAS TO FULFILL CUSTOMS CLEARANCE PROCEDURES NECESSARY FOR IMPORT.

Nevertheless, in case the parties desire to incorporate, partially or as a whole, the expenses paid for goods importation within the liabilities of seller, such preference shall be clarified with an explicit provision duly added to sales agreement.This term can only be used in case the goods will be delivered by sea-freight or inland or multi-vehicle transport and through unloading from ship to quay at the port of destination. Nevertheless, if the parties want to incorporate within liabilities of seller any damages and expenses about the transport of goods from the quay to the port or any other place, the terms DDU or DDP should be employed.

DELIVERED DUTY UNPAID (DDU)

In this method, the delivery responsibility of seller ends once the goods are rendered disposable at the prescribed location in import country. Seller has to undertake any risks and expenses with respect to carriage of goods to such location and to fulfillment of necessary customs procedures (except for taxes, levies and duties payable for import).The buyer has to cover additional expenses and risks due to goods not cleared from customs for import in due time. In case the parties want the seller to fulfill customs procedures and to undertake all possible relevant expenses and risks, they have to concretize such intention through well-articulated expressions.In case the parties want to add to liabilities of seller certain expenses necessary for importation of goods (such as VAT), they have to concretize such intention through well-articulated expressions. This term can be employed regardless of mode of transport.

DELIVERED DUTY PAID (DDP)

Pursuant to this procedure, the delivery liability of seller ends once the goods are rendered disposable at the prescribed location in import country. The seller has to cover all risks and expenses, including any necessary tax, levy and duty with respect to carriage of goods to such location and their clearance at customs. The method DDP signifies maximum seller responsibility, in contrary to EXW method.

DAP HAS REPLACED PREVIOUS DAF, DES AND DDU

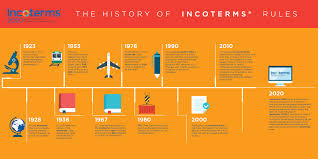

“Delivery at Place” rule signifies that the seller delivers the goods to the disposal of buyer once the vehicle arrives at prescribed destination and without unloading them from such vehicle.It means provision (delivery) of goods to the buyer at a certain point so as to be unloaded from transport vehicle. DAP has replaced previous DAF, DES, and DDU methods. In other words, DAP means the goods are left to the disposal of buyer at transport vehicle at unloading location (a port quay, customs point, airport) and ready for unloading, pursuant to prior agreement between buyer and seller. Buyer covers all customs procedures, expenses, as well as customs-related taxes, levies and duties. Seller undertakes costs and terminal connection damage risks during transport of goods to the prescribed location.On 27 September 2010, ICC issued and updated these rules under Incoterms 2010. The revision came into effect as of 1 January 2011. In Incoterms 2010, the number of delivery modes is decreased from 13 to 11. Four modes are removed, while two new delivery types are established. Besides, INCOTERMS are divided in two general categories. The rules, which cover all transport types, are divided in seven, namely, EXW – FCA – CPT – CIP – DAT – DAP – DDP; whereas FAS – FOB – CFR – CIF are grouped as “exclusive rules for seafreight and inland transport”, with essential amendments in their content.